The real estate market in 2024 is undergoing significant changes, driven primarily by rising mortgage rates. These shifts are impacting buyers, sellers, investors, and the overall market landscape. Understanding these dynamics is crucial for anyone involved in real estate. This article explores how rising mortgage rates are reshaping the market and what this means for different stakeholders.

1. The Current Mortgage Rate Landscape

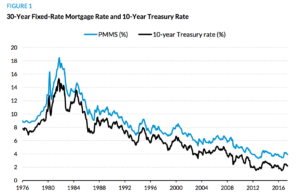

As of 2024, mortgage rates have seen a consistent upward trend. Factors contributing to this rise include inflationary pressures, central bank policies, and economic uncertainties. The Federal Reserve’s efforts to curb inflation by increasing interest rates have directly influenced mortgage rates, making borrowing more expensive.

2. Impact on Homebuyers

Affordability Challenges

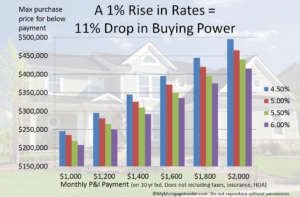

Higher mortgage rates have a direct impact on home affordability. As interest rates rise, the cost of borrowing increases, leading to higher monthly mortgage payments. This has resulted in many potential buyers being priced out of the market or reconsidering their home purchase decisions.

Shift in Buyer Demographics

With the rise in borrowing costs, there is a noticeable shift in the demographics of homebuyers. Younger buyers and first-time homebuyers are particularly affected, as they often have limited financial resources and are more sensitive to changes in interest rates. Consequently, the market is seeing a larger proportion of older, wealthier buyers who can afford higher payments or pay in cash.

3. Effect on Home Sellers

Price Adjustments

Sellers are feeling the impact of rising mortgage rates through slower sales and increased inventory. To attract buyers, many sellers are adjusting their pricing strategies. Price reductions are becoming more common, and the days of multiple offers and bidding wars are waning.

Extended Time on Market

Homes are staying on the market longer as buyers become more cautious and selective. This extended time on market can lead to further price reductions and increased carrying costs for sellers, adding pressure to sell quickly.

4. Influence on Real Estate Investors

Investment Strategy Shifts

Real estate investors are also adapting to the new interest rate environment. Higher mortgage rates mean higher financing costs, which can erode profit margins. As a result, investors are becoming more strategic, focusing on high-yield properties or those with potential for significant appreciation.

Increased Rental Demand

On the flip side, rising mortgage rates are boosting the rental market. As more potential buyers are unable to afford homeownership, the demand for rental properties is increasing. This shift is beneficial for investors who own rental properties, as they can expect higher occupancy rates and potentially higher rents.

5. Regional Market Variations

The impact of rising mortgage rates is not uniform across all regions. Markets with higher price points and those that experienced significant price appreciation in recent years are more susceptible to rate increases. Conversely, more affordable markets may see less dramatic changes but will still be affected by the overall economic environment.

Urban vs. Suburban Markets

Urban markets, which typically have higher property prices, are experiencing more pronounced effects from rising rates. In contrast, suburban and rural areas, where properties are generally more affordable, are seeing a slower impact. However, as remote work trends continue, some suburban areas are experiencing increased demand, somewhat offsetting the impact of higher rates.

6. Long-term Market Outlook

Potential for Market Stabilization

While the immediate effects of rising mortgage rates are challenging, there is potential for market stabilization in the long term. As the market adjusts, prices may stabilize, and new buyers could enter the market at lower price points. Additionally, if inflationary pressures ease, there could be a gradual reduction in mortgage rates, providing some relief to the market.

Adaptation and Innovation

The real estate market is known for its resilience and adaptability. Rising mortgage rates may spur innovation in financing options, such as adjustable-rate mortgages or new loan products designed to make homeownership more accessible. Additionally, technology and data analytics will continue to play a crucial role in helping buyers, sellers, and investors make informed decisions in a changing market.

Conclusion

Rising mortgage rates in 2024 are reshaping the real estate market in significant ways. From altering buyer demographics to influencing seller strategies and investor decisions, the impacts are widespread. Understanding these dynamics is essential for navigating the current market and making informed real estate decisions. As the market continues to adapt, stakeholders must stay informed and agile to thrive in this evolving landscape.

{kind=link}